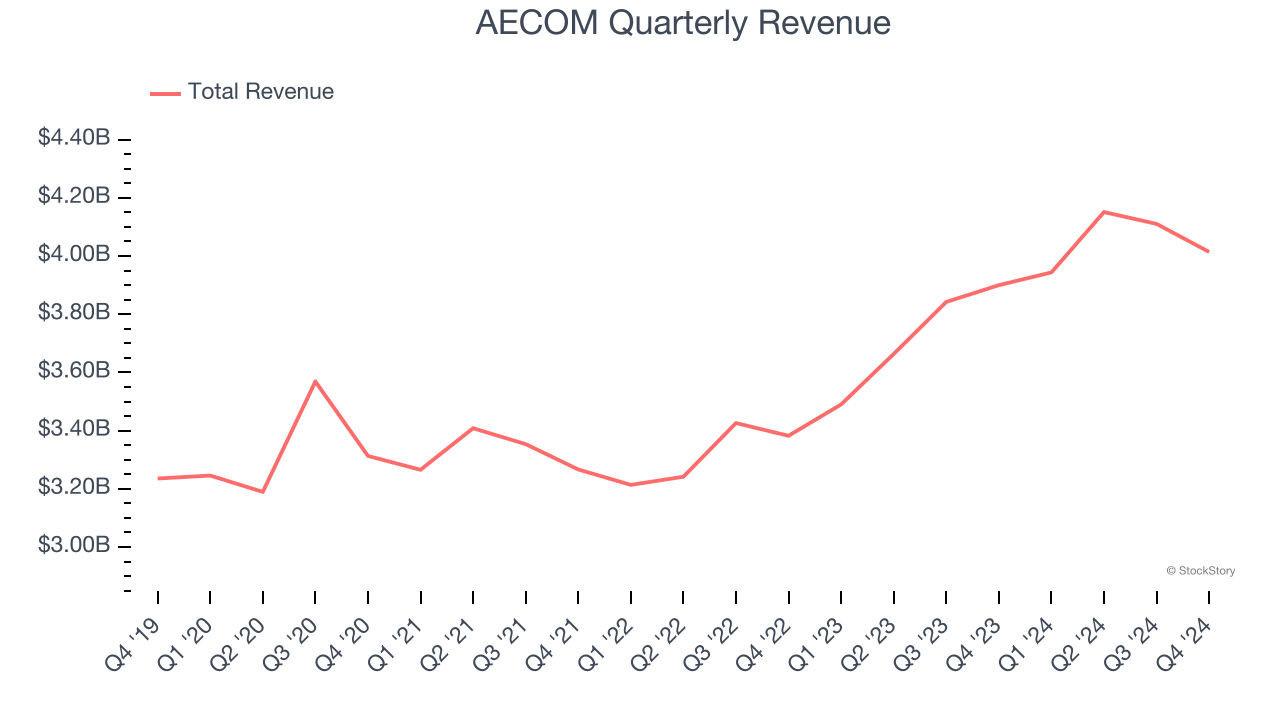

Infrastructure consulting service company AECOM (NYSE:ACM) fell short of the market’s revenue expectations in Q4 CY2024 as sales rose 2.9% year on year to $4.01 billion. Its non-GAAP profit of $1.31 per share was 18.6% above analysts’ consensus estimates.

Is now the time to buy AECOM? Find out by accessing our full research report, it’s free.

AECOM (ACM) Q4 CY2024 Highlights:

- Revenue: $4.01 billion vs analyst estimates of $4.11 billion (2.9% year-on-year growth, 2.3% miss)

- Adjusted EPS: $1.31 vs analyst estimates of $1.10 (18.6% beat)

- Adjusted EBITDA: $271 million vs analyst estimates of $268.3 million (6.8% margin, 1% beat)

- Management slightly raised its full-year Adjusted EPS guidance to $5.13 at the midpoint

- EBITDA guidance for the full year is $1.19 billion at the midpoint, in line with analyst expectations

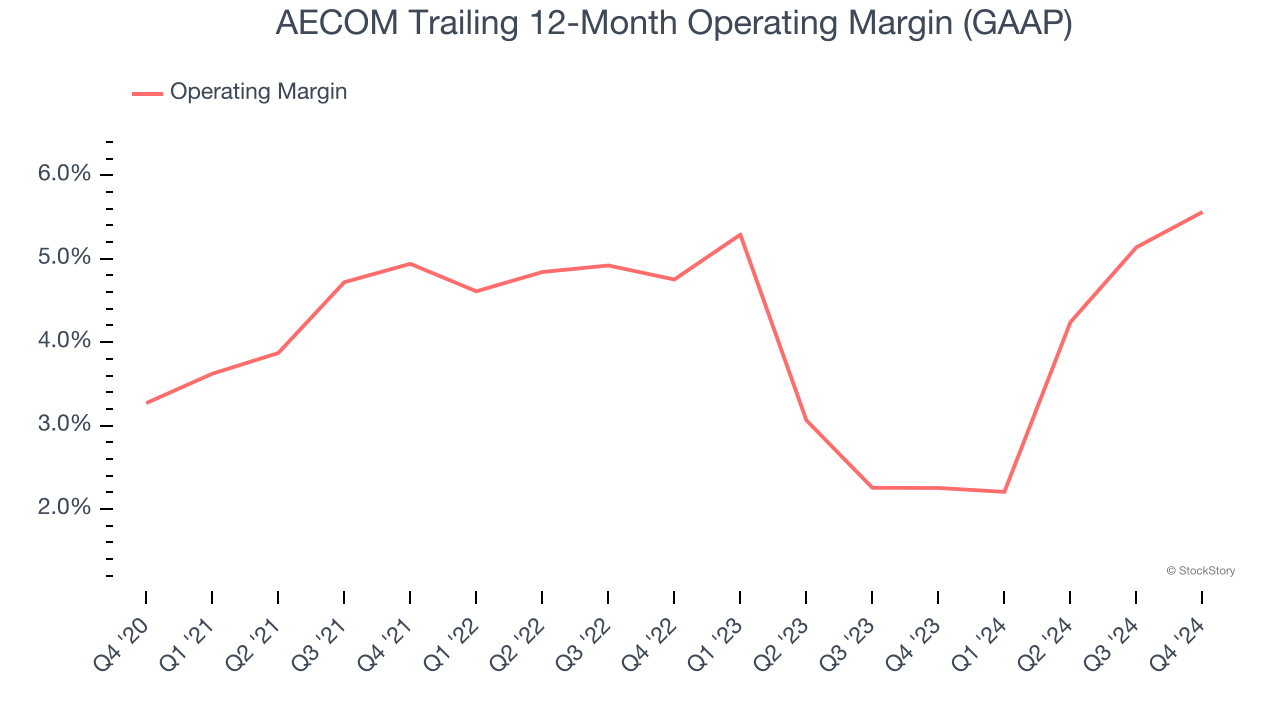

- Operating Margin: 5.9%, up from 4.2% in the same quarter last year

- Free Cash Flow Margin: 2.8%, similar to the same quarter last year

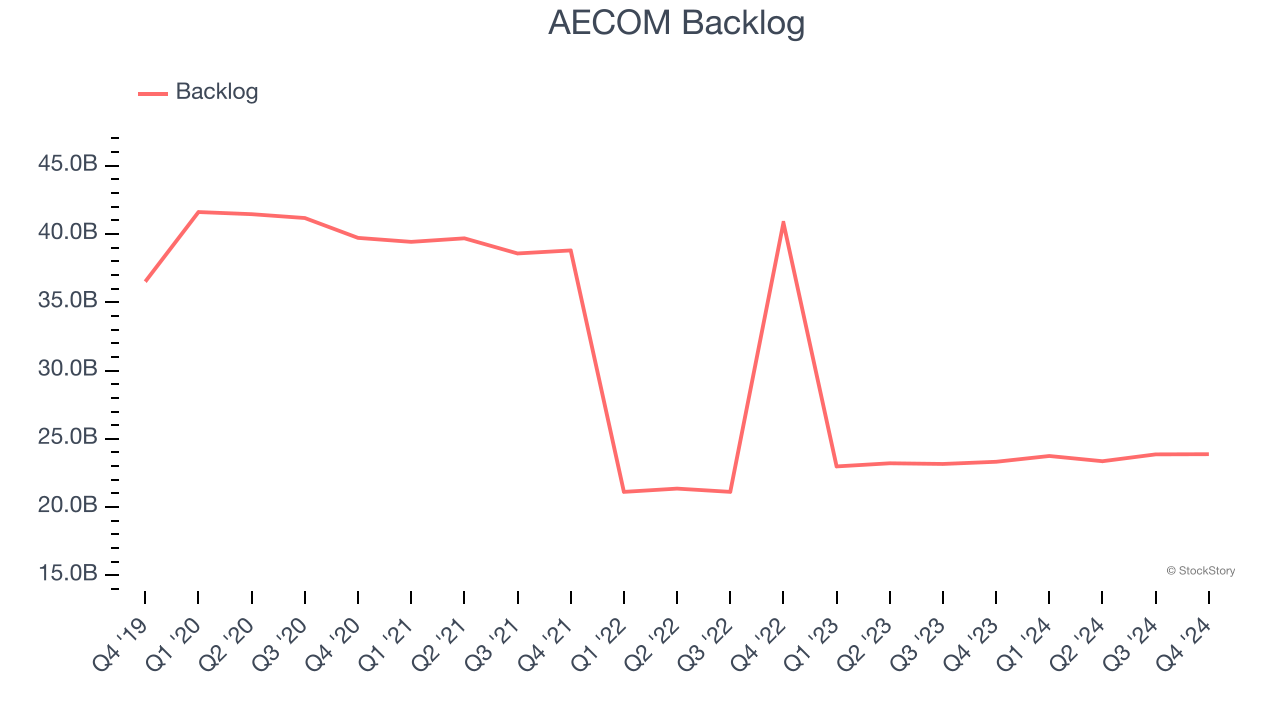

- Backlog: $23.88 billion at quarter end, up 2.4% year on year

- Market Capitalization: $13.99 billion

“Trends across our markets remain robust, and our backlog and pipeline are at record levels, characterized by a highly diverse mix of clients and sectors,” said Troy Rudd, AECOM’s Chief Executive Officer.

Company Overview

Founded in 1990 when a group of engineers from five companies decided to merge, AECOM (NYSE:ACM) provides various infrastructure consulting services.

Engineering and Design Services

Companies providing engineering and design services boast ever-evolving technical expertise. Compared to their counterparts who manufacture and sell physical products, these companies can also pivot faster to more trending areas due to their smaller physical asset bases. Green energy and water conservation, for example, are current themes driving incremental demand in this space. On the other hand, those providing engineering and design services are at the whim of construction and infrastructure project volumes, which tend to be cyclical and can be impacted heavily by economic factors such as interest rates.

Sales Growth

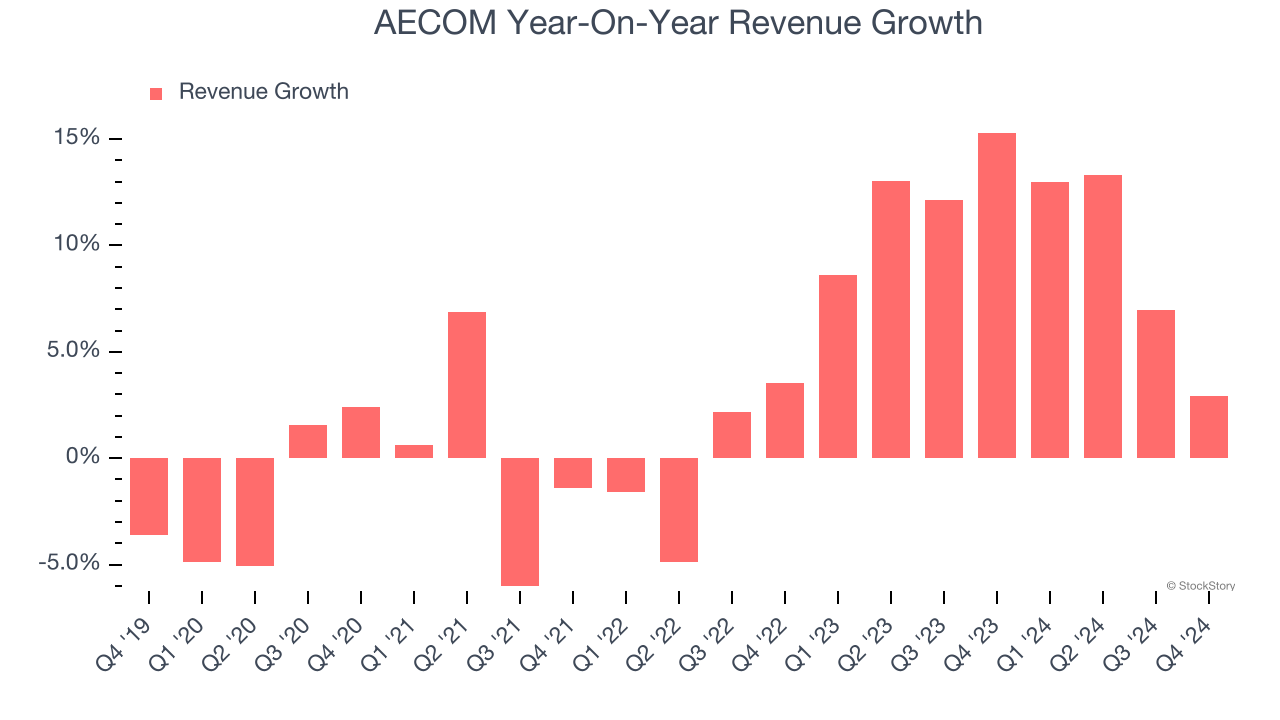

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can have short-term success, but a top-tier one grows for years. Regrettably, AECOM’s sales grew at a sluggish 3.7% compounded annual growth rate over the last five years. This was below our standard for the industrials sector and is a rough starting point for our analysis.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. AECOM’s annualized revenue growth of 10.6% over the last two years is above its five-year trend, suggesting its demand recently accelerated.

AECOM also reports its backlog, or the value of its outstanding orders that have not yet been executed or delivered. AECOM’s backlog reached $23.88 billion in the latest quarter and was flat over the last two years. Because this number is lower than its revenue growth, we can see the company fulfilled orders at a faster rate than it added new orders to the backlog. This implies AECOM was operating efficiently but raises questions about the health of its sales pipeline.

This quarter, AECOM’s revenue grew by 2.9% year on year to $4.01 billion, falling short of Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 6.9% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and indicates its products and services will face some demand challenges.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

Adjusted Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

AECOM was profitable over the last five years but held back by its large cost base. Its average operating margin of 4.2% was weak for an industrials business. This result isn’t too surprising given its low gross margin as a starting point.

On the plus side, AECOM’s operating margin rose by 2.3 percentage points over the last five years.

In Q4, AECOM generated an operating profit margin of 5.9%, up 1.7 percentage points year on year. The increase was encouraging, and since its operating margin rose more than its gross margin, we can infer it was recently more efficient with expenses such as marketing, R&D, and administrative overhead.

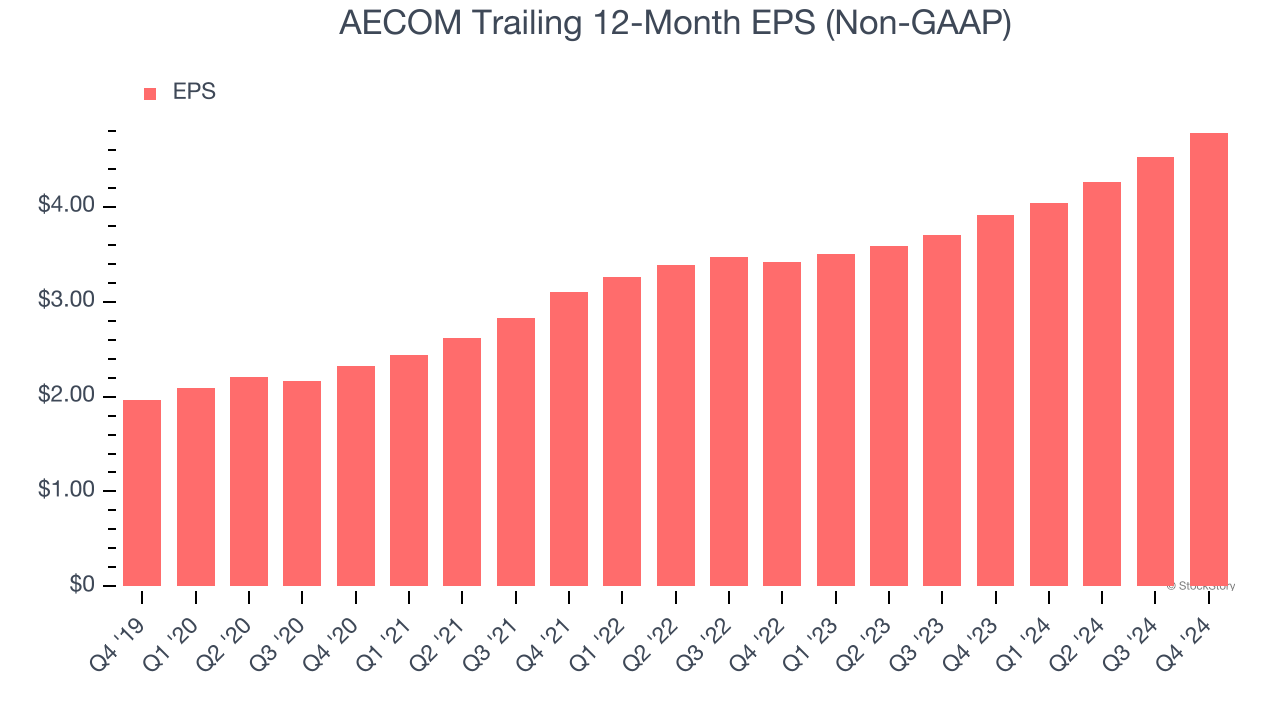

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

AECOM’s EPS grew at an astounding 19.4% compounded annual growth rate over the last five years, higher than its 3.7% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

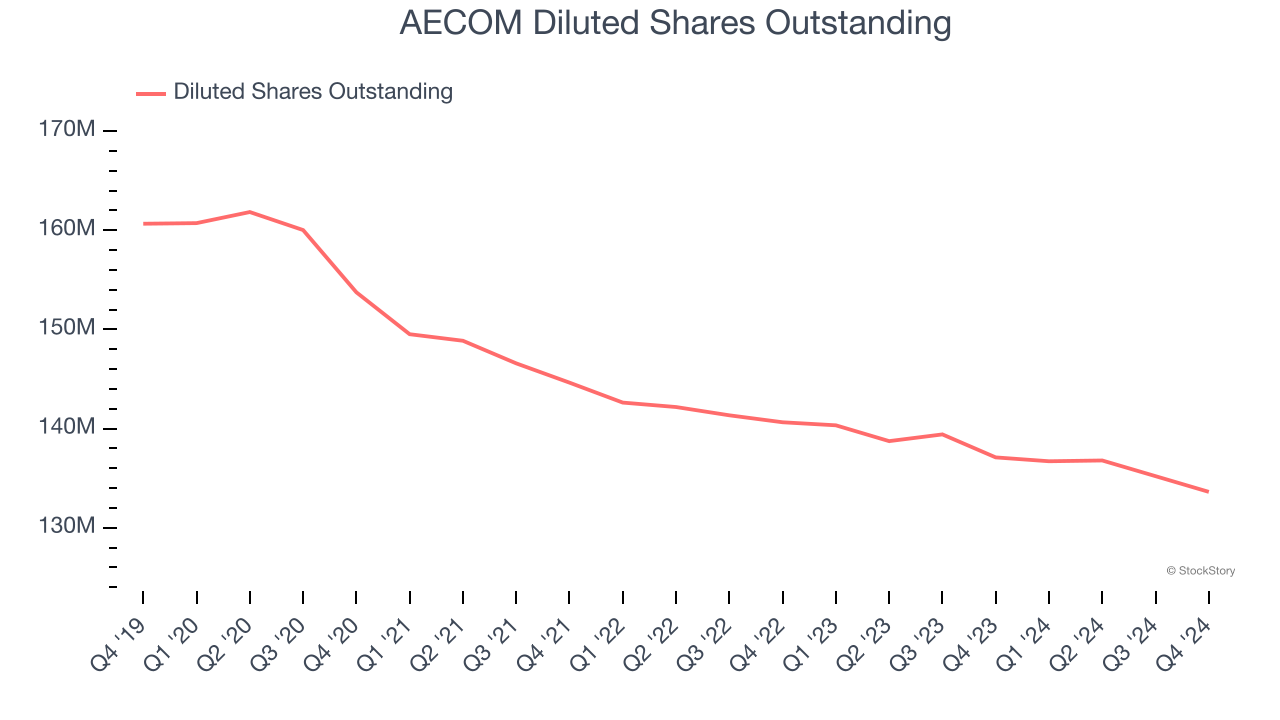

Diving into the nuances of AECOM’s earnings can give us a better understanding of its performance. As we mentioned earlier, AECOM’s operating margin expanded by 2.3 percentage points over the last five years. On top of that, its share count shrank by 16.8%. These are positive signs for shareholders because improving profitability and share buybacks turbocharge EPS growth relative to revenue growth.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For AECOM, its two-year annual EPS growth of 18.2% was lower than its five-year trend. We still think its growth was good and hope it can accelerate in the future.

In Q4, AECOM reported EPS at $1.31, up from $1.05 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects AECOM’s full-year EPS of $4.78 to grow 8.2%.

Key Takeaways from AECOM’s Q4 Results

We enjoyed seeing AECOM exceed analysts’ EPS and EBITDA expectations this quarter. We were also happy it raised its full-year EPS guidance. On the other hand, its revenue missed. Overall, this was still a decent quarter. The stock traded up 2% to $106 immediately after reporting.

So do we think AECOM is an attractive buy at the current price? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.