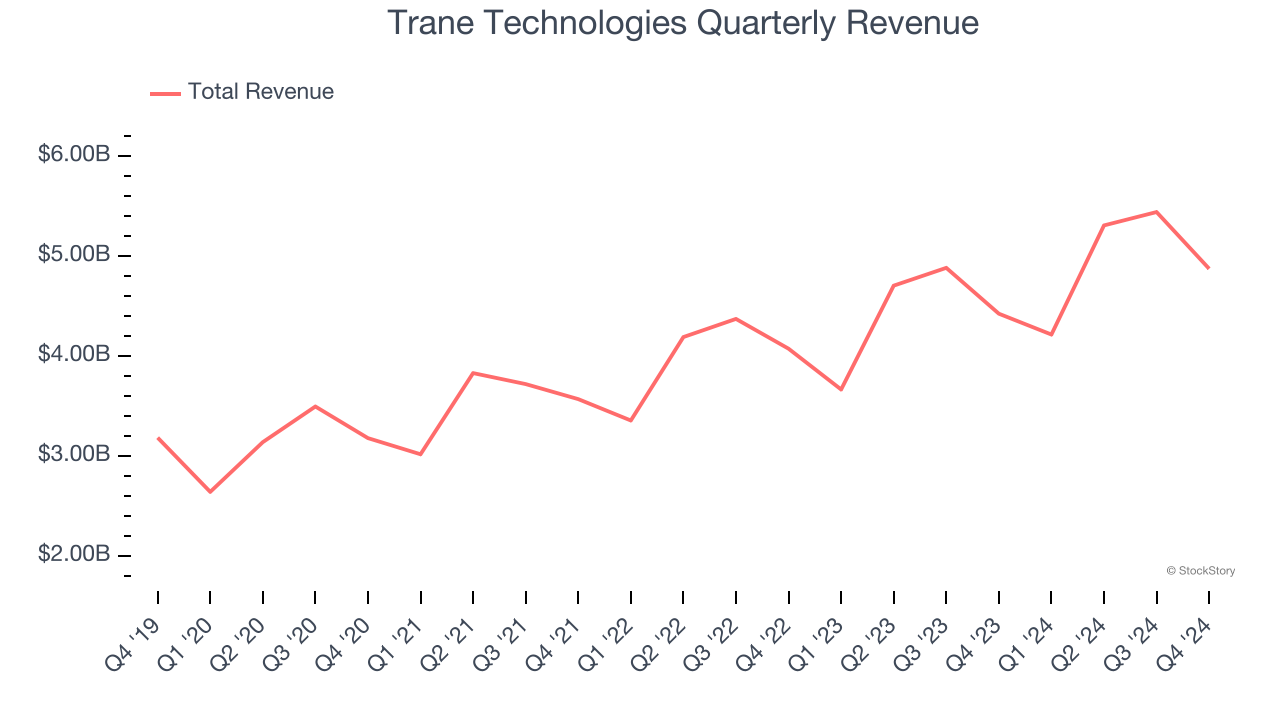

HVAC company Trane (NYSE:TT) reported Q4 CY2024 results beating Wall Street’s revenue expectations, with sales up 10.2% year on year to $4.87 billion. Its non-GAAP profit of $2.61 per share was 2.7% above analysts’ consensus estimates.

Is now the time to buy Trane Technologies? Find out by accessing our full research report, it’s free.

Trane Technologies (TT) Q4 CY2024 Highlights:

- Revenue: $4.87 billion vs analyst estimates of $4.78 billion (10.2% year-on-year growth, 1.9% beat)

- Adjusted EPS: $2.61 vs analyst estimates of $2.54 (2.7% beat)

- Adjusted EBITDA: $894 million vs analyst estimates of $860.7 million (18.3% margin, 3.9% beat)

- Adjusted EPS guidance for the upcoming financial year 2025 is $12.80 at the midpoint, beating analyst estimates by 1.1%

- Operating Margin: 16.6%, up from 15.5% in the same quarter last year

- Market Capitalization: $81.91 billion

Company Overview

With low-pressure heating systems as the first product, Trane (NYSE:TT) designs, manufactures, and sells HVAC and refrigeration systems, the former to commercial and residential building customers and the latter to commercial truck manufacturers.

HVAC and Water Systems

Many HVAC and water systems companies sell essential, non-discretionary infrastructure for buildings. Since the useful lives of these water heaters and vents are fairly standard, these companies have a portion of predictable replacement revenue. In the last decade, trends in energy efficiency and clean water are driving innovation that is leading to incremental demand. On the other hand, new installations for these companies are at the whim of residential and commercial construction volumes, which tend to be cyclical and can be impacted heavily by economic factors such as interest rates.

Sales Growth

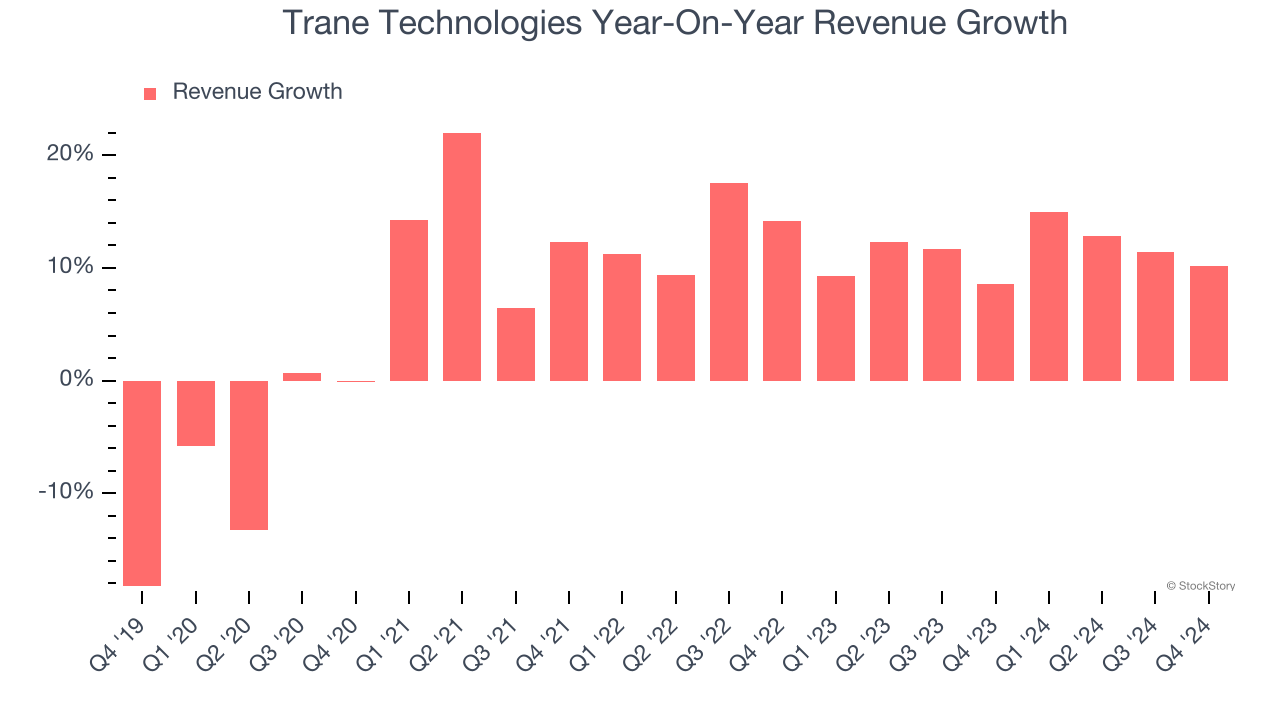

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Thankfully, Trane Technologies’s 8.7% annualized revenue growth over the last five years was decent. Its growth was slightly above the average industrials company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Trane Technologies’s annualized revenue growth of 11.4% over the last two years is above its five-year trend, suggesting its demand recently accelerated.

This quarter, Trane Technologies reported year-on-year revenue growth of 10.2%, and its $4.87 billion of revenue exceeded Wall Street’s estimates by 1.9%.

Looking ahead, sell-side analysts expect revenue to grow 6.7% over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and indicates its products and services will face some demand challenges. At least the company is tracking well in other measures of financial health.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

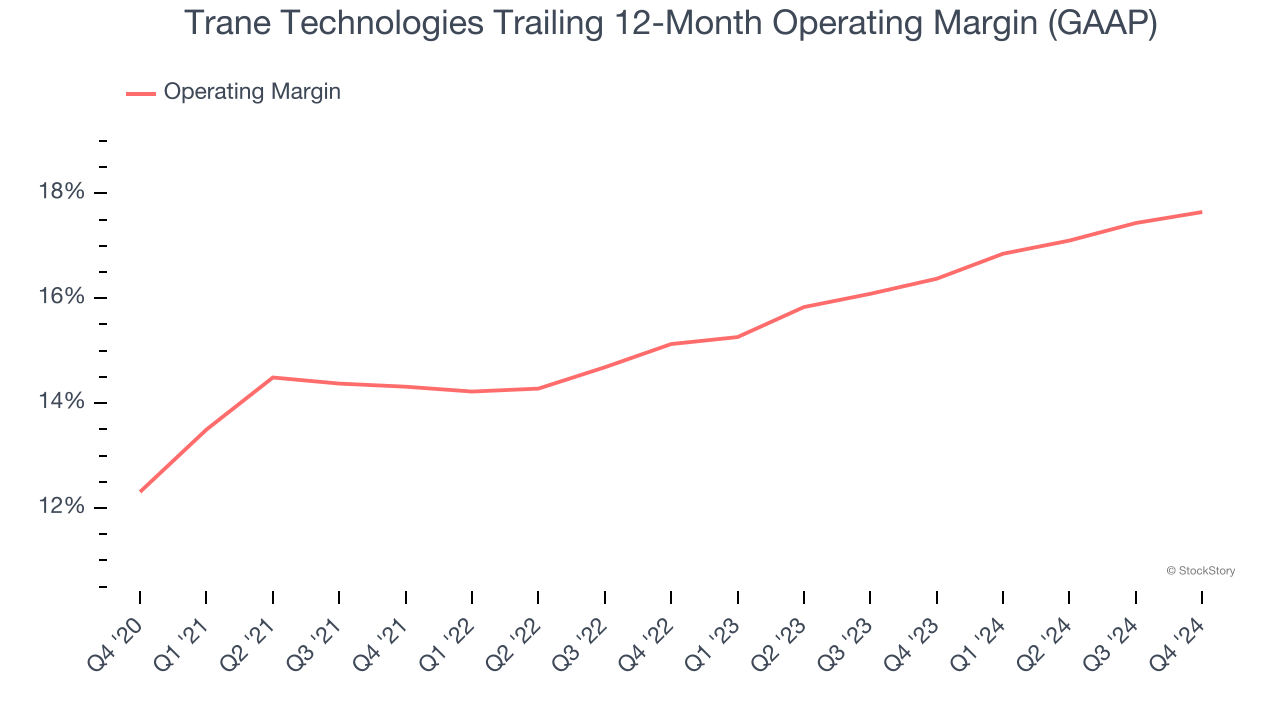

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Trane Technologies has been an optimally-run company over the last five years. It was one of the more profitable businesses in the industrials sector, boasting an average operating margin of 15.4%.

Looking at the trend in its profitability, Trane Technologies’s operating margin rose by 5.3 percentage points over the last five years, as its sales growth gave it immense operating leverage.

This quarter, Trane Technologies generated an operating profit margin of 16.6%, up 1 percentage points year on year. Since its gross margin expanded more than its operating margin, we can infer that leverage on its cost of sales was the primary driver behind the recently higher efficiency.

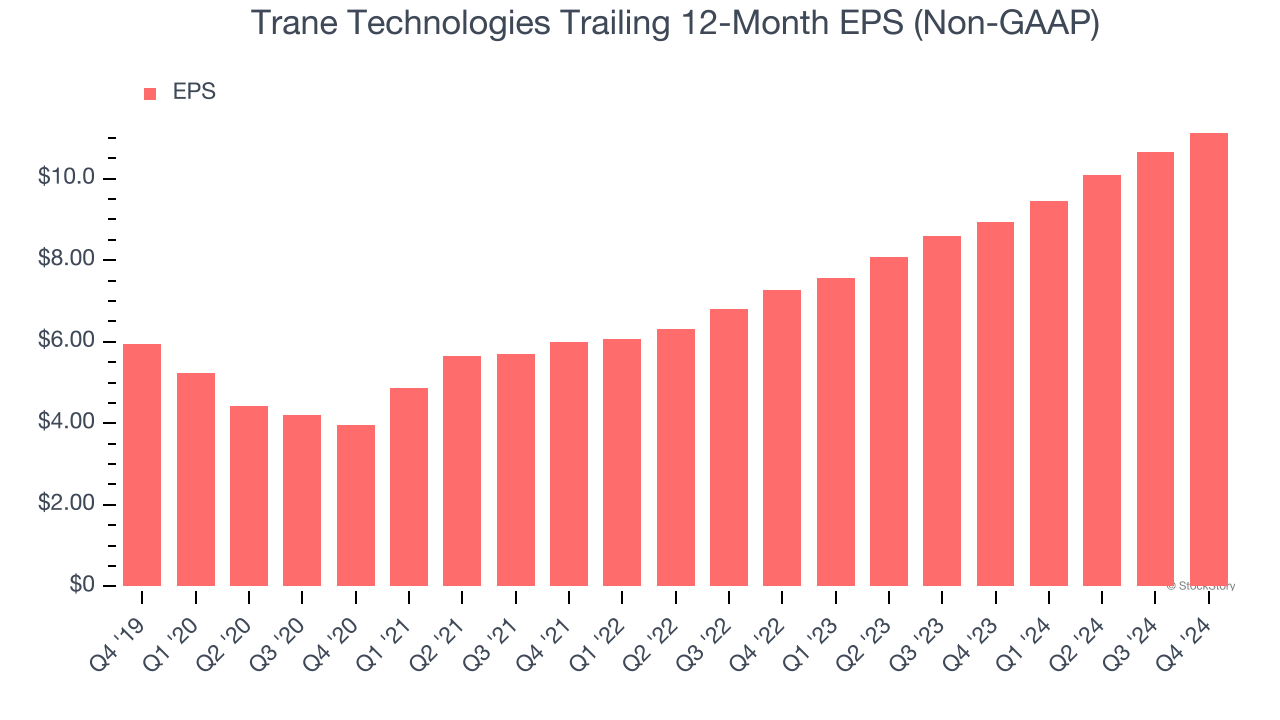

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Trane Technologies’s EPS grew at a remarkable 13.3% compounded annual growth rate over the last five years, higher than its 8.7% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

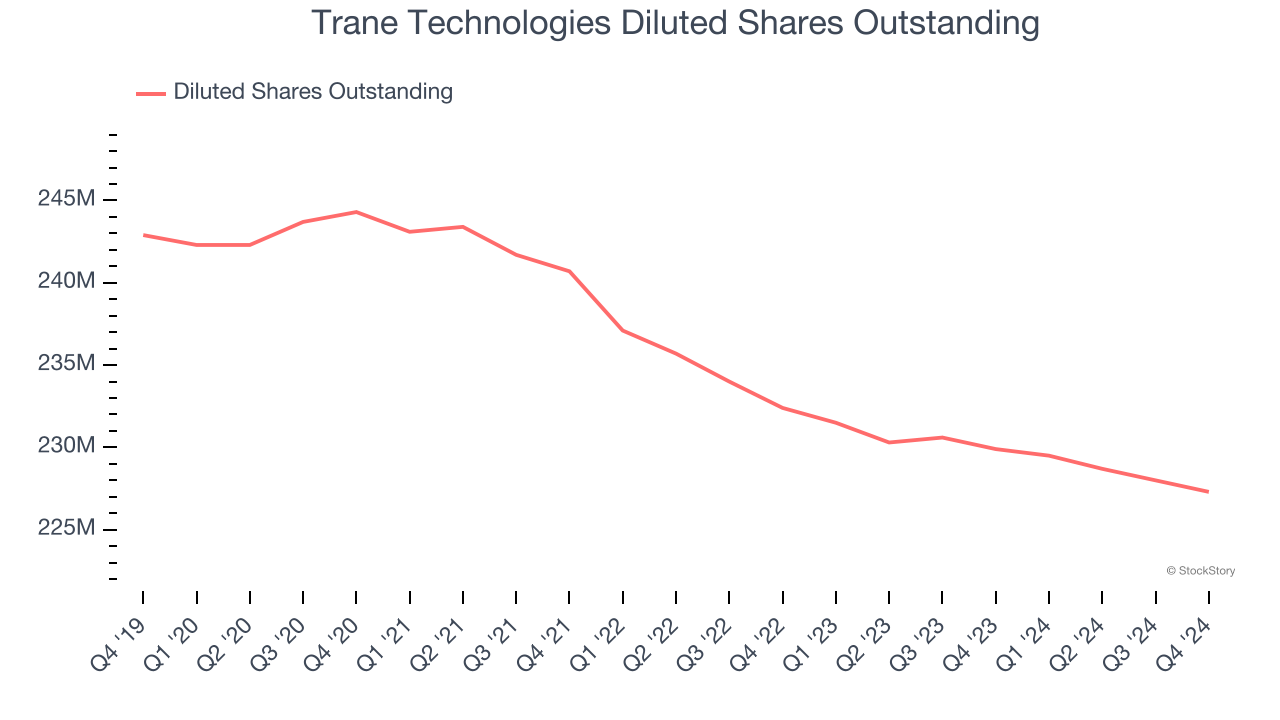

We can take a deeper look into Trane Technologies’s earnings quality to better understand the drivers of its performance. As we mentioned earlier, Trane Technologies’s operating margin expanded by 5.3 percentage points over the last five years. On top of that, its share count shrank by 6.4%. These are positive signs for shareholders because improving profitability and share buybacks turbocharge EPS growth relative to revenue growth.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Trane Technologies, its two-year annual EPS growth of 23.7% was higher than its five-year trend. We love it when earnings growth accelerates, especially when it accelerates off an already high base.

In Q4, Trane Technologies reported EPS at $2.61, up from $2.13 in the same quarter last year. This print beat analysts’ estimates by 2.7%. Over the next 12 months, Wall Street expects Trane Technologies’s full-year EPS of $11.13 to grow 14.1%.

Key Takeaways from Trane Technologies’s Q4 Results

We enjoyed seeing Trane Technologies exceed analysts’ revenue, EBITDA, and EPS expectations this quarter. We were also glad its full-year EPS guidance outperformed Wall Street’s estimates. Overall, we think this was a very solid quarter. The stock traded up 2.4% to $372.84 immediately after reporting.

Trane Technologies put up rock-solid earnings, but one quarter doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.