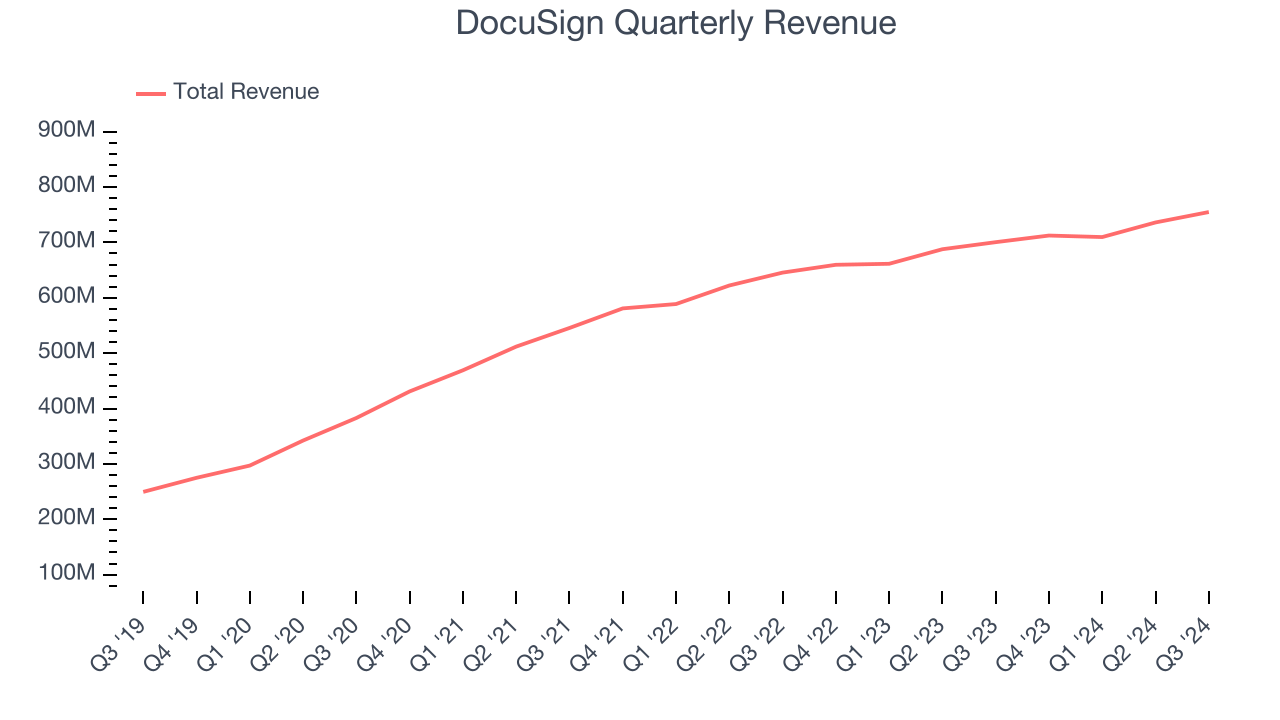

E-signature company DocuSign (DOCU) reported Q3 CY2024 results topping the market’s revenue expectations, with sales up 7.8% year on year to $754.8 million. Guidance for next quarter’s revenue was better than expected at $760 million at the midpoint, 0.5% above analysts’ estimates. Its non-GAAP profit of $0.90 per share was 3% above analysts’ consensus estimates.

Is now the time to buy DocuSign? Find out by accessing our full research report, it’s free.

DocuSign (DOCU) Q3 CY2024 Highlights:

- Revenue: $754.8 million vs analyst estimates of $745.3 million (7.8% year-on-year growth, 1.3% beat)

- Adjusted EPS: $0.90 vs analyst estimates of $0.87 (3% beat)

- Adjusted Operating Income: $223.1 million vs analyst estimates of $216.9 million (29.6% margin, 2.9% beat)

- Raised full year guidance for billings, revenue, operating income

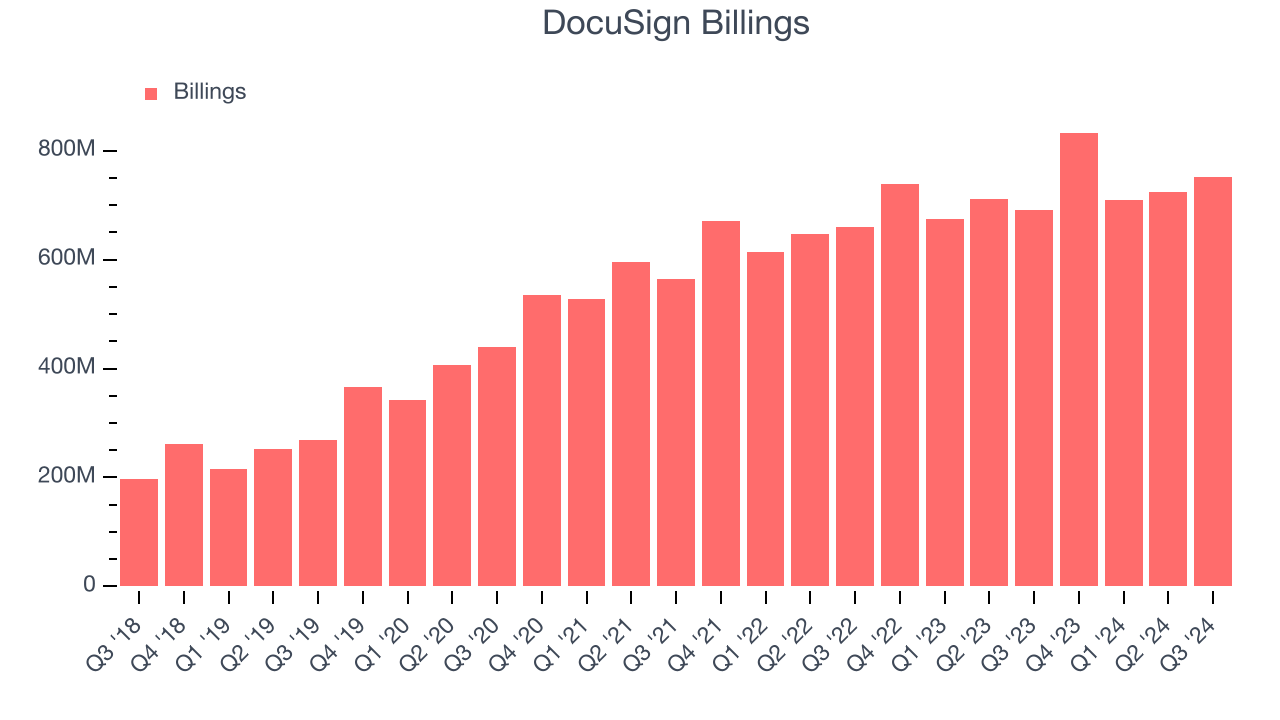

- Billings Guidance for Q4 CY2024 is $875 million at the midpoint, exceeding analyst estimates by 1.5%

- Revenue Guidance for Q4 CY2024 is $760 million at the midpoint, roughly in line with what analysts were expecting

- Operating Margin: 7.8%, up from 2.8% in the same quarter last year

- Free Cash Flow Margin: 27.9%, up from 26.9% in the previous quarter

- Billings: $752.3 million at quarter end, up 8.7% year on year

- Market Capitalization: $17.05 billion

Company Overview

Founded by Seattle-based entrepreneur Tom Gonser, DocuSign (NASDAQ:DOCU) is the pioneer of e-signature and offers software as a service that allows people and organisations to sign legally binding documents electronically.

Document Management

The catch phrase "digital transformation" originally referred to the digitization of documents within enterprises. The growth of digital documents has spurred an explosion of collaboration within and between businesses, which in turn is driving the demand for e-signature and content management platforms.

Sales Growth

A company’s long-term sales performance signals its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Over the last three years, DocuSign grew its sales at a 14.2% compounded annual growth rate. Although this growth is solid on an absolute basis, it fell short of our benchmark for the software sector.

This quarter, DocuSign reported year-on-year revenue growth of 7.8%, and its $754.8 million of revenue exceeded Wall Street’s estimates by 1.3%. Company management is currently guiding for a 6.7% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 5.5% over the next 12 months, a deceleration versus the last three years. This projection is underwhelming and suggests its products and services will face some demand challenges.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

Billings

Billings is a non-GAAP metric that is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

DocuSign’s billings came in at $752.3 million in Q3, and over the last four quarters, its growth was underwhelming as it averaged 7.1% year-on-year increases. This performance mirrored its total sales and suggests that increasing competition is causing challenges in acquiring/retaining customers.

Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period measures the months a company needs to recoup the money spent on acquiring a new customer. This metric helps assess how quickly a business can break even on its sales and marketing investments.

DocuSign’s recent customer acquisition efforts haven’t yielded returns as its CAC payback period was negative this quarter, meaning its sales and marketing investments outpaced its revenue. The company’s inefficiency indicates it operates in a highly competitive environment where there is little differentiation between DocuSign’s products and its peers.

Key Takeaways from DocuSign’s Q3 Results

This was a beat and raise quarter, with the company exceeding analyst estimates on billings, revenue, and operating profit. Next quarter's billings guidance came in ahead and full year guidance was lifted for billings, revenue, and operating profit. Overall, we think this was still a very solid quarter with some key areas of upside. The stock traded up 17% to $97.94 immediately after reporting.

Indeed, DocuSign had a rock-solid quarterly earnings result, but is this stock a good investment here? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.