Industrial component provider Timken (NYSE:TKR) met Wall Street’s revenue expectations in Q3 CY2024, but sales fell 1.4% year on year to $1.13 billion. Its non-GAAP profit of $1.23 per share was 10.6% below analysts’ consensus estimates.

Is now the time to buy Timken? Find out by accessing our full research report, it’s free.

Timken (TKR) Q3 CY2024 Highlights:

- Revenue: $1.13 billion vs analyst estimates of $1.12 billion (in line)

- Adjusted EPS: $1.23 vs analyst expectations of $1.38 (10.6% miss)

- EBITDA: $190 million vs analyst estimates of $199.3 million (4.7% miss)

- Management lowered its full-year Adjusted EPS guidance to $5.60 at the midpoint, a 8.2% decrease

- Gross Margin (GAAP): 30.6%, in line with the same quarter last year

- Operating Margin: 13%, in line with the same quarter last year

- EBITDA Margin: 16.9%, down from 18.9% in the same quarter last year

- Free Cash Flow Margin: 7.8%, down from 13.2% in the same quarter last year

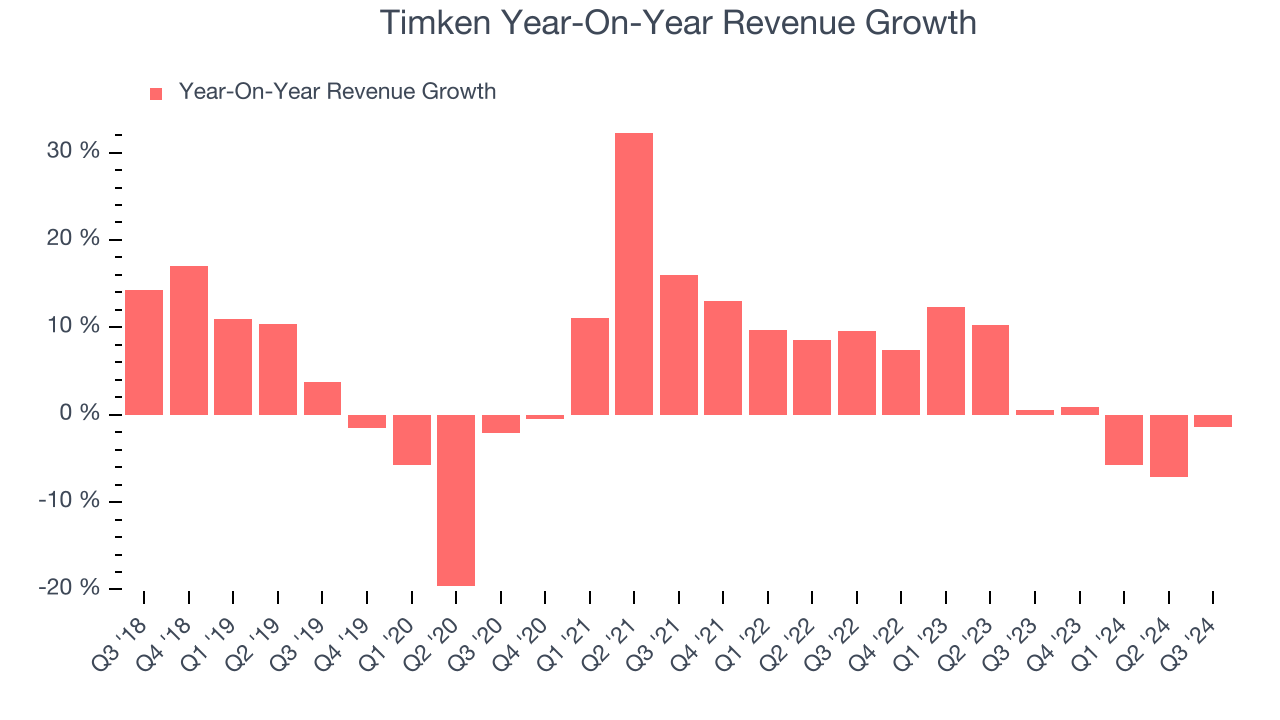

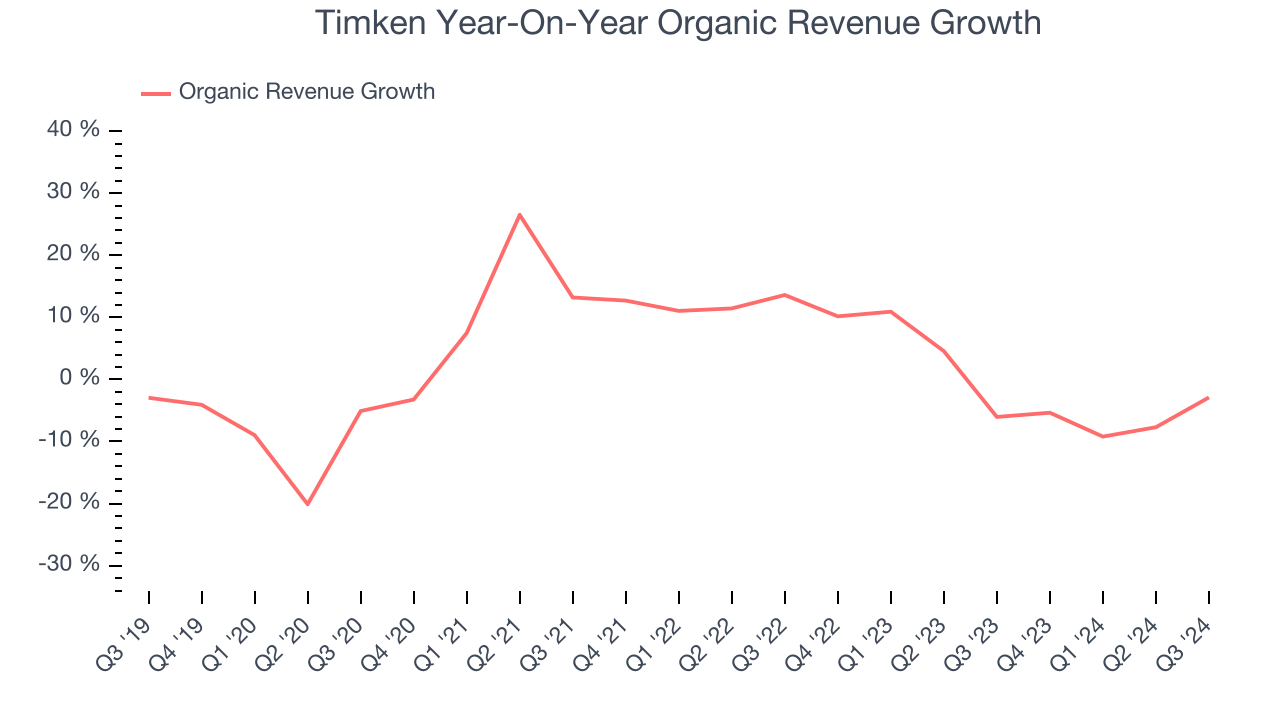

- Organic Revenue fell 2.9% year on year (-6% in the same quarter last year)

- Market Capitalization: $5.85 billion

"It is an honor to be part of the talented Timken team as we work to accelerate profitable growth and customer-centric innovation," said Tarak Mehta, president and chief executive officer.

Company Overview

Established after the founder noticed the difficulty freight wagons had making sharp turns, Timken (NYSE:TKR) is a provider of industrial parts used across various sectors.

Engineered Components and Systems

Engineered components and systems companies possess technical know-how in sometimes narrow areas such as metal forming or intelligent robotics. Lately, automation and connected equipment collecting analyzable data have been trending, creating new demand. On the other hand, like the broader industrials sector, engineered components and systems companies are at the whim of economic cycles. Consumer spending and interest rates, for example, can greatly impact the industrial production that drives demand for these companies’ offerings.

Sales Growth

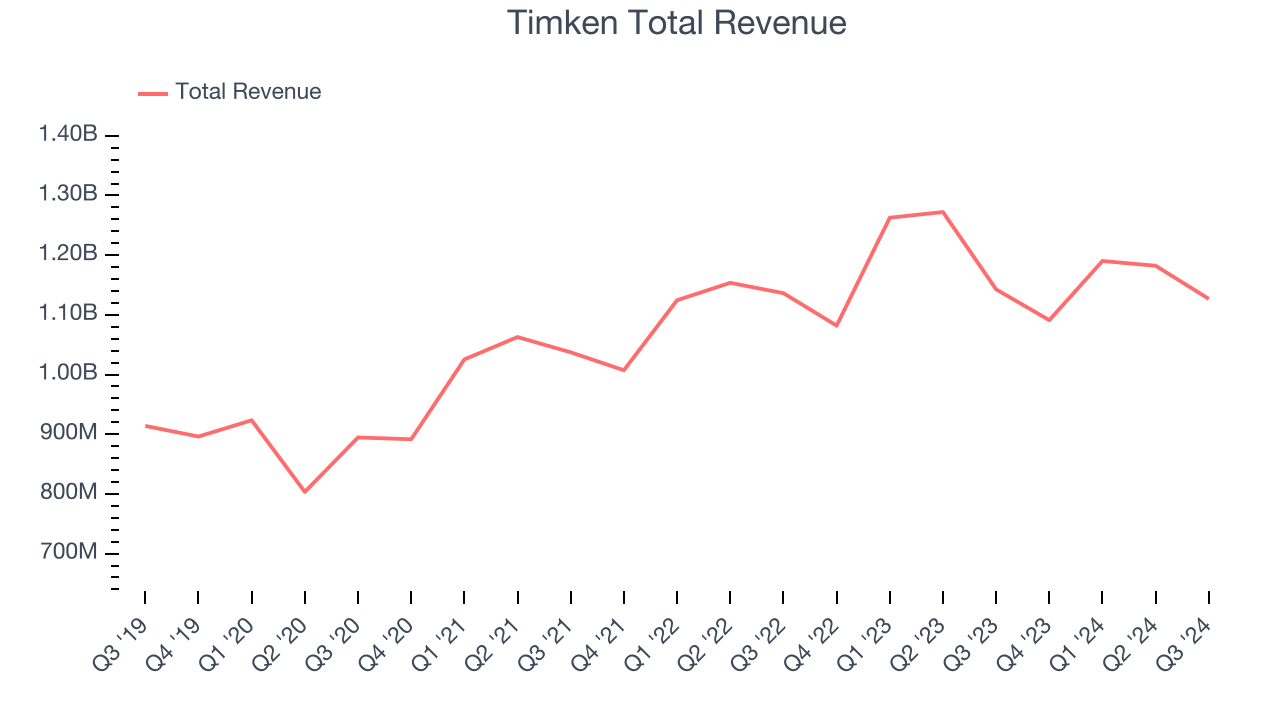

A company’s long-term performance can give signals about its business quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Regrettably, Timken’s sales grew at a sluggish 3.8% compounded annual growth rate over the last five years. This shows it failed to expand in any major way, a rough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Timken’s recent history shows its demand slowed as its annualized revenue growth of 1.9% over the last two years is below its five-year trend.

We can better understand the company’s sales dynamics by analyzing its organic revenue, which strips out one-time events like acquisitions and currency fluctuations because they don’t accurately reflect its fundamentals. Over the last two years, Timken’s organic revenue was flat. Because this number is lower than its normal revenue growth, we can see that some mixture of acquisitions and foreign exchange rates boosted its headline performance.

This quarter, Timken reported a rather uninspiring 1.4% year-on-year revenue decline to $1.13 billion of revenue, in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 3% over the next 12 months, an improvement versus the last two years. While this projection shows the market thinks its newer products and services will fuel better performance, it is still below the sector average.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefitting from the rise of AI, available to you FREE via this link.

Operating Margin

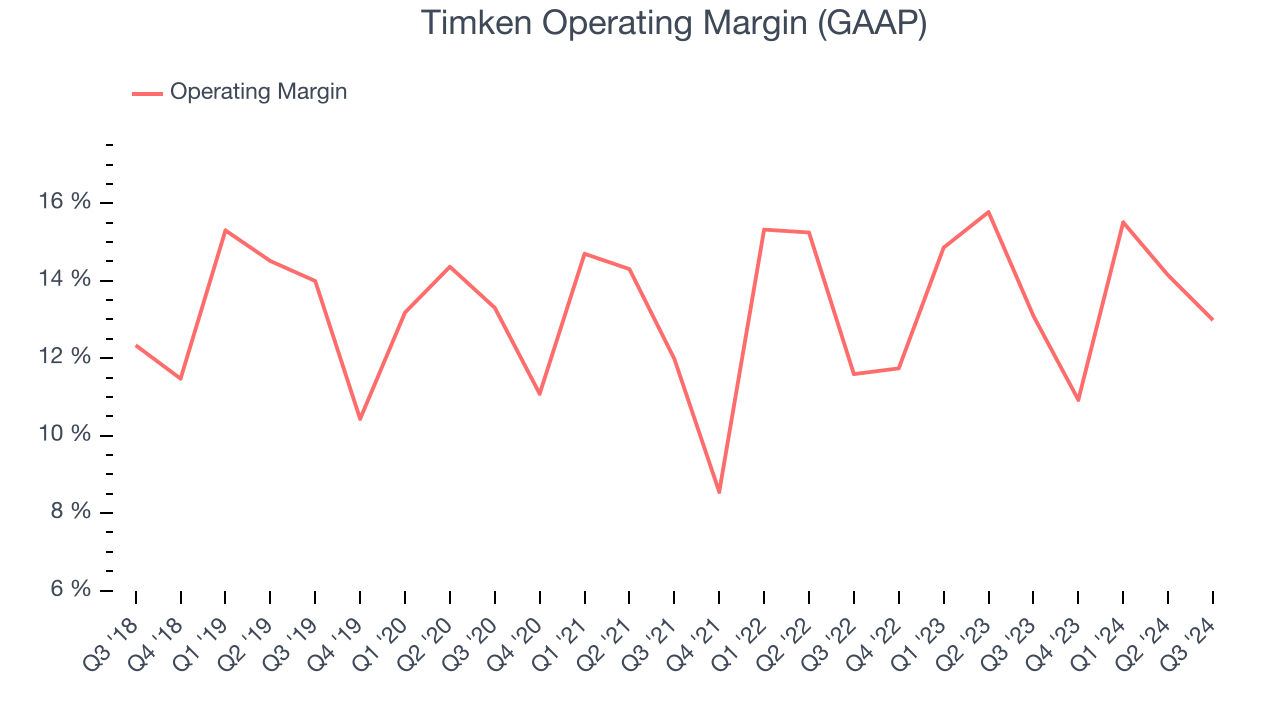

Timken has been an optimally-run company over the last five years. It was one of the more profitable businesses in the industrials sector, boasting an average operating margin of 13.3%. This result was particularly impressive because of its low gross margin, which is mostly a factor of what it sells and takes huge shifts to move meaningfully. Companies have more control over their operating margins, and it’s a show of well-managed operations if they’re high when gross margins are low.

Analyzing the trend in its profitability, Timken’s annual operating margin might have seen some fluctuations but has generally stayed the same over the last five years, highlighting the long-term consistency of its business.

In Q3, Timken generated an operating profit margin of 13%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

Earnings Per Share

Analyzing revenue trends tells us about a company’s historical growth, but the long-term change in its earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Timken’s unimpressive 4.7% annual EPS growth over the last five years aligns with its revenue performance. This tells us it maintained its per-share profitability as it expanded.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

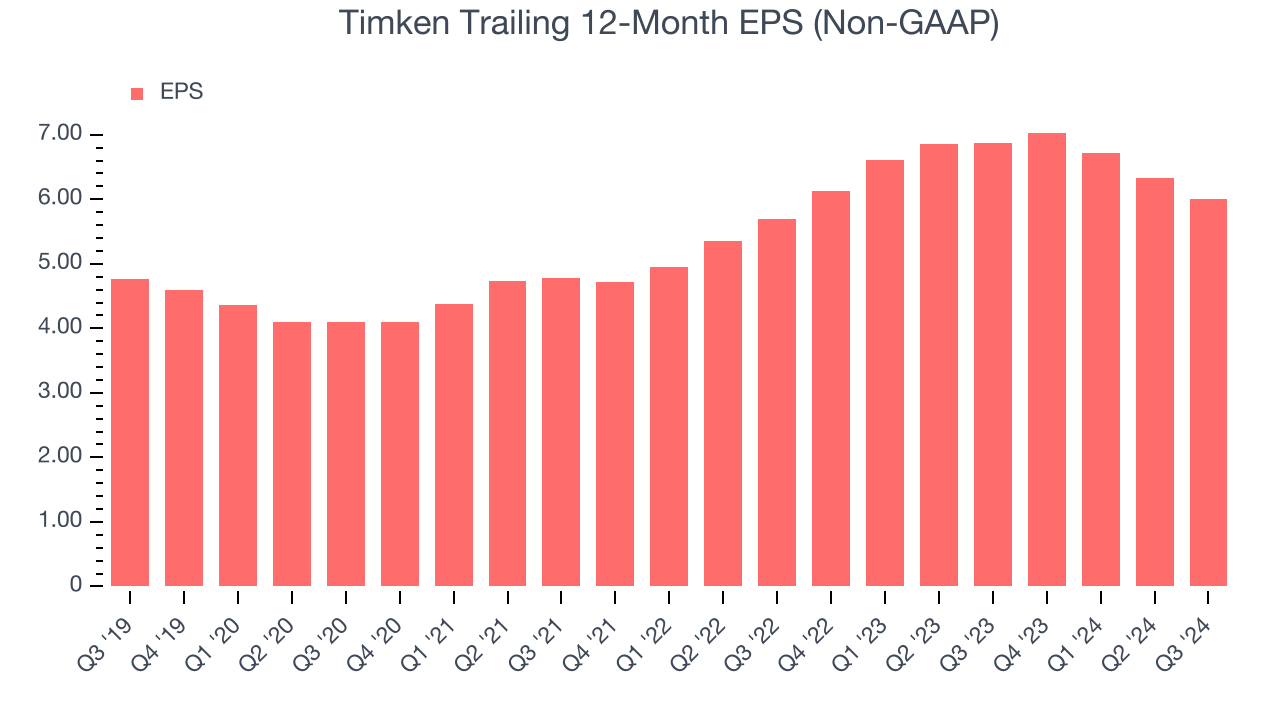

For Timken, its two-year annual EPS growth of 2.7% was lower than its five-year trend. We hope its growth can accelerate in the future.In Q3, Timken reported EPS at $1.23, down from $1.55 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street expects Timken’s full-year EPS of $6.00 to grow by 11.7%.

Key Takeaways from Timken’s Q3 Results

It was good to see Timken beat analysts’ revenue expectations this quarter. On the other hand, its EPS forecast for the full year missed and its EPS fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 5.1% to $79.10 immediately after reporting.

Timken underperformed this quarter, but does that create an opportunity to invest right now? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.