Since making a second run into the $50’s two years ago, Lucid Group Inc. (NASDAQ: LCID) has been a ‘clear’ loser.

On Friday, shares of the California-based luxury electric vehicle (EV) maker skidded to a fresh all-time low of $2.97 — extending a dreadful reversal from their February 2021 peak of $64.86. The 95% plunge has seemingly made the company a hopeless long shot in an EV race being dominated by Elon Musk’s Tesla and China’s BYD.

But not so fast.

On Thursday, Lucid announced that it produced 2,391 vehicles in the fourth quarter of 2023, a 54% increase from the third quarter of 2023. Thanks to bigger discounts, deliveries also improved sequentially, albeit at a slower pace (19%) to 1,734 . For all of 2023, production and deliveries reached 8,428 and 6,001, respectively. Both the quarterly and full year figures are significantly below 2022 levels, but the Q3 to Q4 improvement suggests Lucid may be closer to an inflection point.

Like other high-end EV players, the company has been slowed by tough macroeconomic conditions that have placed its vehicles well outside the budget for most Americans. Although Lucid’s affluent customer base is relatively immune to inflation, moderating inflation in 2024 could attract more upper-middle income consumers to the premium brand. A downturn in interest rates, as the stock market has anticipated in recent weeks, would lower new auto loan rates and potentially help expand the pool of those in the market for a top of the line EV.

With this said, it will likely take more than a strengthening U.S. economy to change Lucid’s fortunes. Although deliveries to customers have finally begun, the corresponding financial results have been murky.

It hasn’t helped matters that CFO Sherry House resigned in December 2023 to pursue other opportunities. With a replacement yet to be named, the news has added another layer of uncertainty to an already reeling EV maker.

Staving off bankruptcy

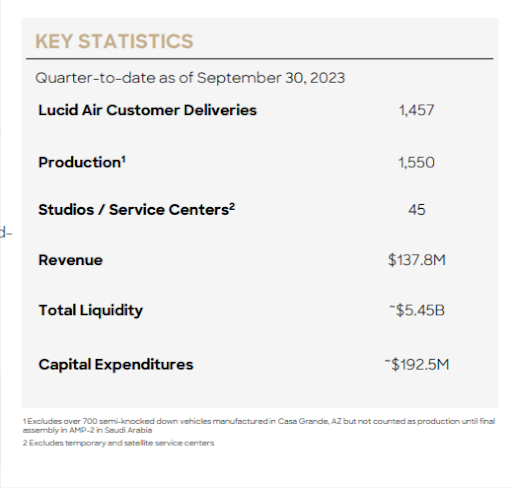

In November 2023, Lucid reported third quarter revenue of $137.8 million. While this lagged the $150.9 million of revenue recorded in the second quarter of 2023 (and was accompanied by a $631 million loss), it wasn’t the most disappointing part of the press release. Management sharply lowered its 2023 production guidance from more than 10,000 vehicles to 8,000 to 8,500 vehicles. The change was made to more “prudently align (production) with deliveries” but emitted the vibe that demand was falling short of expectations.

There was, however, a silver lining in the third quarter report that the market has yet to give Lucid credit for. The company ended the period with approximately $5.45 billion in liquidity. This marked a significant uptick from the $4.6 billion of cash available at the end of the second quarter. It also means that Lucid’s cash position now represents 74% of its current $7.4 billion market capitalization. In other words, the market is giving the company virtually no credit for future growth and the stock is trading near liquidation value.

More importantly, the $5.45 billion in liquidity is expected to keep Lucid’s motor running at least through 2025. At a time when several EV challengers are conceding or facing bankruptcy, this is worth something. Lucid will be around for a while and still has time to right the ship.

Range is a big selling point

Lucid will face an extremely difficult and competitive landscape in 2024 as EV models become more mainstream and car buyers have more choices than ever before. A year ago, there were about 40 electric cars, trucks and SUVs available in the United States. Today there are approximately 140. Hundreds more are available in international markets.

This means Lucid’s inaugural Air sedan will have to beat out many other car buyer options even in the smaller luxury category. One way it plans to win is to offer a variety of price points. Its current lineup includes:

- The Lucid Air Pure AWD/RWD starting at $74,900. It was recently named to Car & Driver’s ‘10Best List’ for 2024 which is based on value, performance, innovation and overall driving experience.

- The Lucid Air Touring which starts at $85,900.

- The Lucid Air Grand Touring starting at $115,600.

For EV enthusiasts that have a spare quarter million dollars to spend, Lucid also offers Air Sapphire, the world’s first electric super-sports sedan, for $249,000 and up.

The biggest determinant of Lucid’s financial success though may be its Gravity SUV, which was unveiled at the November 2023 L.A. Auto Show and expected to drop in late 2024. One thing Gravity has going for it — a sticker price that is relatively ‘light’ for the luxury category at under $80,000. If U.S. household disposable income trends higher, more consumers could lean towards this type of SUV.

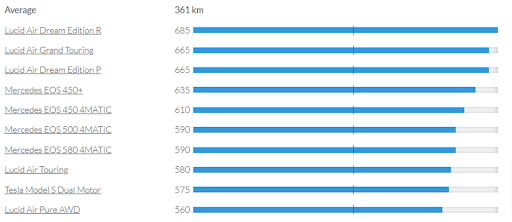

One competitive advantage Lucid will have heading into 2024 is superior driving range. According to EV Database, the company boasts five of the top 10 EVs by mileage. The Gravity SUV is projected to have a range of over 440 miles. For EV buyers that prioritize range and infrequent charging, Lucid’s high-end range technology could make it worth the high-end price.

Production ramping in anticipation of demand

Among the criticisms Lucid has faced is limited manufacturing capacity. Since its 2007 founding, vehicle production has exclusively centered on its factory in Casa Grande, Arizona. This is starting to change.

In September 2023, the company began assembling Lucid Airs at its new Advanced Manufacturing Plant ‘AMP-2’ in Jeddah, Saudi Arabia. It is the first ever car manufacturing plant to open in the country.

For Lucid, it comes with the potential for a huge ramp in production capacity. The facility’s initial phase will enable the assembly of 5,000 vehicles annually en route to future production of up to 155,000 vehicles per year.

Lucid was able to break ground in Jeddah as part of an agreement to support the country’s electric transportation goals. The Saudi Green Initiative is targeting EVs to account for 30% of new car sales by 2030.

Oversold conditions have set in

Lucid’s vehicles may not be selling out, but its equity shares sure are. From a technical analysis perspective, the stock has faced immense selling pressure since spiking to $17.81 in January 2023. This was sparked by a bullish Citigroup report that predicted Tesla challengers like Lucid, Rivian and Nio will gain ground. The market has long forgotten about this call, however, and Lucid’s depressed technical indicators tell the story.

On the daily chart, the Relative Strength Indicator (RSI) is at 7. An RSI reading below 30 generally indicates that a stock is oversold or undervalued. Out of 1,745 U.S.-listed large- and mid-cap stocks, LCID ranks dead last in terms of the momentum oscillator. It is also trading well below the lower Bollinger Band, a trendline that when breached can point to oversold conditions.

Does this mean LCID can only go up from here? It depends who you ask.

Technical analysts would probably argue that LCID has limited downside from here. The charts certainly suggest the upside/downside ratio is favorable. Fundamentals-driven Wall Street research analysts would beg to differ.

On Thursday, CFRA downgraded LCID to a Strong Sell, giving the stock a scathing $1.00 price target that implies 67% more downside. The analyst cautioned investors to avoid the temptation of buying the low priced penny stock, referring to it as a “falling knife.” The same day Cantor Fitzgerald reiterated its Hold rating.

This continued a pattern of Street skepticism around LCID that persisted throughout 2023. Among nine analysts that actively follow the stock, 8 are neutral and 1 is still bearish. Interestingly though, the group’s average price target ($5.00) equates to more than 60% upside. More reason to believe market sentiment is overly bearish.

Is an epic short squeeze down the road?

Despite Lucid’s trip to a new low, short sellers see more pain ahead — or from their perspective, more gains ahead. Roughly 27% of the stock’s 874 million share float is held short. It is one of the top 10 most short U.S. mid-caps (polarizing stocks like Carvana and C3.ai still take the cake). This confirms just how far out of favor LCID has fallen.

But it also means the short squeeze powder keg is loaded.

If Lucid’s news flow turns bullish, things could change in a hurry. An uptrend could easily be accelerated by shorts sellers buying to cover their positions. In isolation, short squeeze potential isn't a reason to bet on a stock — but in the case of LCID, it’s certainly part of the appeal.

A potential near-term catalyst for the stock is the company’s fourth quarter update scheduled for after the market close on February 21st. If management offers a bullish 2024 outlook or announces some sort of other positive surprise, traders could flock to the stock. It’s unlikely, but given the history of occasional flare ups, it’s always a possibility. If LCID does rally, a high-volume push past long-term resistance at $4.25 could turbocharge the EV maker out of penny stock land.

Bottom Line

Fifteen years since its founding, Lucid Motors has finally started to deliver EVs to customers — but has failed to deliver convincing financial results and shareholder returns. The former SPAC turned penny stock faces an uphill battle in an increasingly crowded EV market but has superior driving range technology and increased capacity on its side. Progress towards carving out a meaningful slice of a global EV market forecast to top $600 billion this year could spark renewed buying interest in LCID.