Options data and analytics provider moves to implied yield curve and replaces LIBOR with leading overnight rates in options implied volatility and Greek calculations for North America, Europe, Asia Pacific

OptionMetrics, an options database and analytics provider for institutional investors and academic researchers worldwide, is announcing its new options implied methodology, offering even greater accuracy in options calculations in the U.S., Europe, Asia Pacific. OptionMetrics replaces the zero curve (used by other providers) with its implied yield curve, constructed with a term structure of overnight rates and implied risk-free rates from options on major indices, for more accurate implied volatility, forward price, index dividend, and borrow rate calculations.

This press release features multimedia. View the full release here: https://www.businesswire.com/news/home/20220208005115/en/

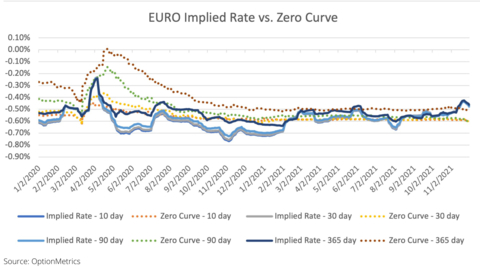

Pictured in this chart are the implied rates (solid line) versus the zero curve rates (dotted line) for the Euro from January 2020 through December 2021. The chart illustrates how OptionMetrics’ new options implied methodology, constructed with a term structure of implied risk-free rates from options on major indices, offers greater accuracy over those based on zero curve rates (typically used by other providers) in options calculations such as implied volatility, forward price, index dividend, borrow rate and others. In applying leading overnight rates from the options market (such as with SOFR replacing LIBOR) and data from index options, OptionMetrics’ methodology more accurately reflects the cost of borrowing and lending in the options markets in Europe, North America and Asia Pacific. (Graphic: Business Wire)

In leveraging data from index options, OptionMetrics more accurately reflects costs of borrowing and lending in options markets. The methodology reduces implied volatility spreads and offers true volatility and Greek calculations compared to leveraging private bank lending rates or other measures that may include credit risk or unrealistic borrowing assumptions.

Overnight rates, such as SOFR, are also used in the methodology for options expiring in less than 30 days to reduce noise associated with short-dated contracts. As the new standard over LIBOR, SOFR also has nearly zero credit risk exposure.

OptionMetrics constructs term structures of implied rates curves for the:

- Dollar using SOFR (Secured Overnight Financing Rate) and S&P 500 Index options,

- Swiss Franc using SARON (Swiss Average Rate Overnight) and SMI Index options,

- Euro using ESTR (Euro Short-Term Rate) overnight rates and EUROSTOXX 50 options,

- British Pound using SONIA (Sterling Overnight Index Average) and FTSE 100 options,

- Yen using TONAR (Tokyo Overnight Average Rate) and Nikkei 225 options.

OptionMetrics applies a specialized smoothing filter to remove noise from estimates.

“At OptionMetrics, we are committed to ensuring the most accurate options data, Greeks, and implied volatility calculations. Our options implied methodology draws from the options market to more accurately reflect borrowing and lending risks, continuing our strategy to provide the most accurate data to backtest strategies and assess risk,” said OptionMetrics CEO David Hait, Ph.D.

Volatilities are automatically calculated with the new rates across OptionMetrics’ IvyDB US, IvyDB Europe, IvyDB Asia Pacific, and IvyDB Global Indices. No changes are made to table format, file naming, historical calculations.

Email info@optionmetrics.com for more.

View source version on businesswire.com: https://www.businesswire.com/news/home/20220208005115/en/

Contacts

Hilary McCarthy

Clearpoint Agency

774.364.1440

Hilary@clearpointagency.com